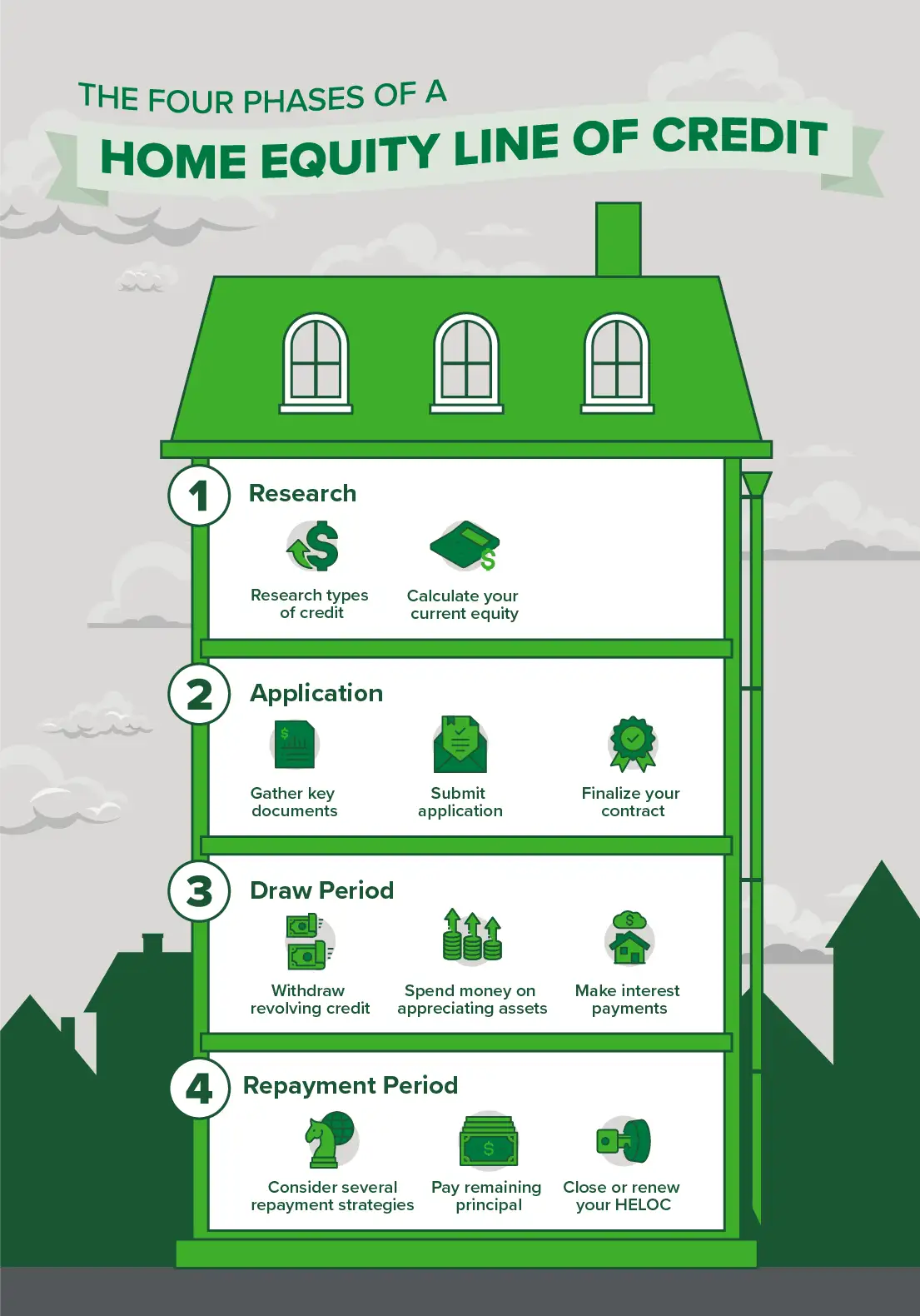

When considering a Home Equity Line of Credit (HELOC), understanding interest-only payment options is crucial. A key financial decision hinges on the implications of these payments.

Interest-only payments on a HELOC represent a repayment strategy where borrowers make monthly payments covering only the accrued interest on the outstanding loan balance. Principal repayment is deferred. For example, if the outstanding balance is $50,000 and the interest rate is 6%, monthly interest payments could be around $250. This contrasts with a standard repayment plan, which includes both interest and a portion of the principal. This approach can potentially offer short-term financial relief, allowing borrowers to retain more cash flow each month.

The primary benefit of this payment structure is its potential to reduce the immediate financial burden compared to a traditional repayment schedule. However, this comes with the significant long-term implication of accumulating principal. The deferral of principal repayments means that the total interest paid over the life of the loan can potentially increase significantly. Borrowers must carefully consider the long-term financial implications and their ability to repay the full principal amount at a later date. A thorough review of repayment options is critical to assess if this approach aligns with individual financial goals and risk tolerance.

This discussion provides insight into the financial considerations surrounding HELOCs. The next section will explore different repayment strategies and their respective advantages and disadvantages.

HELOC Interest-Only Payments

Understanding HELOC interest-only payments is crucial for informed financial decisions. These payments, a specific repayment strategy, offer distinct short-term and long-term implications.

- Reduced monthly outgoings

- Accumulated principal

- Higher total interest

- Financial flexibility

- Risk assessment

- Loan terms

HELOC interest-only payments initially lower monthly outgoings, but this comes at a cost. Accumulated principal and potentially higher total interest create a long-term financial burden. Financial flexibility is a factor, enabling short-term cash flow management. A thorough risk assessment is essential; borrowers must evaluate their ability to repay the accumulated principal later. Loan terms and associated interest rates will dictate specific payment structures and their consequences. For example, a HELOC with a high interest rate and interest-only payments could lead to a significantly larger total debt over the life of the loan, compared to a lower interest-only rate or a standard repayment plan. Therefore, careful consideration of the various aspects is vital for informed financial choices.

1. Reduced Monthly Outgoings

Reduced monthly outgoings are a key allure of HELOC interest-only payments. The strategy's defining characteristic is the deferral of principal repayment. Consequently, monthly payments primarily cover accrued interest, not the principal. This results in lower initial monthly obligations. For instance, a borrower with a $100,000 HELOC and a 6% interest rate might have significantly lower monthly interest-only payments compared to a comparable loan structured for full principal and interest repayment. This lower monthly burden can be a significant short-term benefit, potentially freeing up cash flow for other financial needs.

The immediate reduction in monthly outgoings can be highly attractive, especially during periods of financial uncertainty or increased expenses. This can provide borrowers with greater financial flexibility. However, the crucial point is that the lower initial payments are achieved by deferring principal repayment. This means the borrower is accumulating principal, and the total interest paid over the life of the loan can be considerably higher than with a traditional repayment plan. Ultimately, the total cost of the loan will be significant, potentially exceeding the total cost under a traditional repayment plan. Understanding the long-term implications of this strategy is essential for responsible financial decision-making.

The seemingly immediate advantage of reduced monthly outgoings under interest-only payment plans on HELOCs must be considered alongside the longer-term financial obligations. While providing temporary cash flow relief, the strategy necessitates a comprehensive understanding of the accumulated principal and the increased total interest expense. Carefully evaluating personal financial capacity and long-term repayment goals is vital to avoid unforeseen and potentially substantial financial burdens in the future.

2. Accumulated Principal

Accumulated principal is a direct consequence of HELOC interest-only payments. This strategy focuses solely on interest payments, deferring the repayment of the principal loan amount. As a result, the outstanding principal balance grows over time. This accrual of principal is significant because it directly impacts the total cost of the loan. While monthly payments might seem lower initially, the eventual repayment obligation increases, potentially substantially, as the principal amount increases.

Consider a scenario where a homeowner utilizes a HELOC with a $50,000 loan balance and an interest rate of 6%. With interest-only payments, the monthly payment might be roughly $250. While this initial payment seems manageable, the principal remains untouched. After a year, the principal will be slightly higher due to interest accruing. This accumulation continues over multiple years. Consequently, the total amount repaid, including interest, will substantially exceed the original loan amount if repayment of principal is not made promptly. Furthermore, if interest rates increase during the period of interest-only payments, the total accumulated interest will be higher than initially expected. Understanding this compounding effect is critical for borrowers to realistically assess the long-term cost and ensure they have a clear plan to repay the accumulated principal balance.

The crucial connection between accumulated principal and HELOC interest-only payments necessitates a proactive approach to repayment planning. Borrowers must carefully evaluate their financial capacity to repay both the accrued interest and the accumulating principal. Failing to adequately plan for the complete repayment of the accumulated principal could lead to significant financial strain down the line. This understanding underscores the importance of responsible borrowing and a thorough financial assessment when considering this payment strategy. A well-defined repayment timeline, realistic income projections, and the ability to consistently address the growing principal amount are key aspects to successfully navigating a HELOC with interest-only payments.

3. Higher Total Interest

HELOC interest-only payments, while potentially offering reduced initial monthly outgoings, often result in a higher total interest paid over the life of the loan. This stems from the deferral of principal repayment, which allows interest to accumulate on the outstanding balance, ultimately increasing the overall cost of the loan.

- Compounding Interest Effect

The core driver of higher total interest is the compounding effect of interest. Interest accrues not only on the initial loan amount, but also on the accumulated interest itself. This exponential growth of interest can significantly amplify the total interest paid over the life of the loan. For example, a modest initial interest rate can lead to a substantially greater interest burden in the long run if the principal isn't repaid promptly.

- Deferred Principal Repayment

With interest-only payments, borrowers avoid the reduction of the principal balance. The accumulated interest is added to the principal balance, creating a larger base upon which future interest accrues. This deferred repayment strategy, while perhaps easing short-term cash flow pressures, compounds the interest owed, leading to a higher overall interest expense compared to a loan with regular principal and interest payments.

- Impact of Interest Rate Fluctuations

Interest rates can fluctuate throughout the life of a HELOC. If rates rise during the interest-only period, the total interest paid escalates further. The accumulating principal amount also becomes more significant, resulting in higher overall costs for the borrower. This variable factor adds another layer of risk to the interest-only payment strategy.

- Comparison to Traditional Repayment

A critical factor in evaluating interest-only payments is contrasting them with traditional loan repayment methods. In a standard repayment plan, a portion of each payment goes toward reducing the principal balance. This reduction in the principal balance reduces the amount subject to interest calculations. Consequently, the total interest accrued under a standard repayment plan, while perhaps higher monthly, often results in a lower overall interest cost in the long run for loans with consistent repayment schedules.

In summary, while HELOC interest-only payments might alleviate immediate financial strain, borrowers must acknowledge the substantial potential for a higher total interest expense. The compounding effect of interest, the deferral of principal, and the potential for interest rate fluctuations all contribute to this outcome. A careful evaluation of financial capacity, long-term goals, and potential interest rate fluctuations is essential before committing to this repayment strategy. Comparing interest-only payments with traditional repayment methods is a crucial step in making an informed financial decision.

4. Financial Flexibility

Financial flexibility, a key component in assessing HELOC interest-only payments, signifies the ability to manage current financial obligations while maintaining a degree of maneuverability for future needs. Interest-only payments on a HELOC can offer immediate financial flexibility by reducing the immediate burden of principal repayment. This reduction in monthly payments can allow for additional funds to be allocated to other financial priorities. The strategy, however, is not without its trade-offs, as the deferral of principal repayment directly impacts long-term financial flexibility. This deferral must be carefully considered, as accumulated interest adds to the overall loan cost and potentially restricts future financial maneuverability. Understanding the relationship between financial flexibility and HELOC interest-only payments is crucial for informed decision-making.

Real-world examples illustrate the duality of financial flexibility presented by this repayment strategy. A business owner facing a significant expansion opportunity might use the lower monthly payments to fund the project while maintaining cash flow for other daily operational needs. Conversely, a homeowner facing unforeseen expenses might find the initial reduced payments beneficial, but the eventual repayment obligations must be factored into future budget projections. The strategic use of HELOC interest-only payments necessitates a comprehensive understanding of the trade-offs and a meticulous plan for repayment and cash flow management. A plan for paying off the increasing principal amount is essential. Prospective borrowers must meticulously analyze their financial situation and assess how this repayment method aligns with their personal financial goals and long-term financial commitments. Failure to accurately account for repayment obligations can jeopardize long-term financial flexibility and lead to unintended consequences.

In conclusion, while HELOC interest-only payments can offer short-term financial flexibility through reduced monthly outgoings, the accumulation of principal and potentially higher total interest necessitates a clear, long-term financial strategy. Prospective borrowers must carefully evaluate their current financial situation, expected future income, and overall financial goals. This crucial assessment will determine whether the short-term flexibility offered is balanced by the long-term ramifications. Financial flexibility in this context is not merely a temporary reduction in payments but a carefully considered aspect of a comprehensive financial plan. A detailed repayment timeline that addresses the accumulated principal and ongoing interest is imperative for maintaining long-term financial flexibility.

5. Risk Assessment

A thorough risk assessment is paramount when considering HELOC interest-only payments. This evaluation is critical to understanding the potential financial ramifications and ensuring the strategy aligns with individual financial capacity and long-term goals. The assessment must extend beyond initial affordability to encompass the accumulating principal, fluctuating interest rates, and the borrower's capacity for full repayment.

- Ability to Repay Accumulated Principal

A primary aspect of risk assessment involves evaluating the borrower's ability to repay the accumulating principal at the stipulated time. Predicting future income, accounting for potential economic downturns, and assessing the impact of unexpected expenses is crucial. For instance, job loss, significant healthcare costs, or unforeseen major repairs could jeopardize the ability to repay the total loan amount, including accrued interest, which is a critical risk to manage. Borrowers must possess a concrete repayment plan that accounts for these eventualities. A thorough analysis of savings, existing debts, and a realistic assessment of future income are essential components of this assessment.

- Interest Rate Fluctuations

Interest rate fluctuations present a significant risk with HELOC interest-only payments. A rise in interest rates during the interest-only period can lead to substantial increases in the overall cost of the loan. Historical data and market trends should be considered. Understanding the potential for rate increases is critical to developing a strategy that mitigates this risk, such as having alternative financial resources available should rates rise significantly. Borrowers should analyze the potential effect of interest rate increases on their monthly payments and evaluate alternative repayment strategies if rates rise above a predetermined threshold.

- Long-Term Financial Stability

A comprehensive risk assessment also requires an evaluation of overall long-term financial stability. The strategy should align with the borrower's overall financial goals and long-term plans. Financial emergencies, unforeseen expenses, and lifestyle changes should be considered when constructing a risk assessment model for HELOC interest-only payments. This evaluation needs to account for potential changes in income, family responsibilities, and other financial obligations. A realistic picture of future financial demands is crucial in determining whether interest-only payments are a sustainable financial choice.

- Comparison with Alternatives

Assessing the risk associated with HELOC interest-only payments requires comparing it to alternative borrowing strategies. Evaluating the overall cost and repayment structure of other options, such as traditional repayment methods, is imperative. Analyzing the repayment terms, interest rates, and overall costs associated with different lending scenarios can help borrowers weigh the risk-reward trade-offs of interest-only payments against alternative financial options.

Ultimately, a thorough risk assessment for HELOC interest-only payments goes beyond a simple calculation of monthly affordability. It necessitates a holistic evaluation of the borrower's ability to repay the accumulated principal, the potential impact of interest rate fluctuations, long-term financial stability, and a comparative analysis with alternative borrowing methods. A sound risk assessment is crucial for a responsible financial decision that aligns with long-term financial goals. Failure to conduct such a comprehensive evaluation can expose borrowers to considerable financial risks, regardless of how attractive the reduced initial monthly payments may seem.

6. Loan Terms

Loan terms significantly influence the viability and implications of HELOC interest-only payments. These terms encompass parameters like interest rates, loan duration, and repayment schedules, all of which directly affect the overall cost and risk associated with the interest-only repayment strategy. A high-interest rate, for instance, can dramatically increase the total interest paid over the life of the loan under an interest-only repayment scheme, even with potentially lower monthly payments initially. Conversely, a shorter loan duration can help to limit the accumulating principal and associated interest cost, although it increases the monthly payment burden. Repayment schedules and their flexibility directly impact the borrower's ability to manage future financial obligations and plan for full repayment.

The relationship between loan terms and interest-only payments extends to the structure of the HELOC itself. Variable interest rates, common in HELOCs, introduce a dynamic factor. If interest rates rise during the interest-only period, the monthly interest payments escalate, increasing the overall cost of borrowing. This variable factor introduces a significant risk that needs thorough consideration. Fixed-rate HELOCs, in contrast, offer a more predictable interest rate structure. Understanding the specific details of the loan terms, including the interest rate type (fixed or variable) and the conditions for modifying repayment plans, is crucial for mitigating associated risks. A longer loan term, for example, potentially implies greater accumulated principal and total interest expense. Real-world examples highlight these intricacies. A borrower with a variable-rate HELOC experiencing a significant rate increase during the interest-only period could be faced with a substantially higher monthly payment burden than initially anticipated, making the strategy less advantageous.

In summary, loan terms are fundamental in evaluating the suitability of HELOC interest-only payments. Understanding the intricacies of interest rates, loan duration, and repayment structures is essential for a comprehensive assessment. Borrowers must analyze the potential effects of variable interest rates, assess the implications of accumulating principal, and compare the strategy's long-term costs against other potential repayment options. A thorough understanding of loan terms is crucial to ensure the chosen repayment strategy aligns with individual financial goals and risk tolerance, ultimately minimizing potential financial strain. The interplay between these various aspects of loan terms and interest-only payments highlights the necessity for careful planning and a thorough understanding of the overall financial implications before committing to this particular repayment strategy.

Frequently Asked Questions About HELOC Interest-Only Payments

This section addresses common questions regarding HELOC interest-only payments. Understanding these nuances is crucial for informed financial decisions.

Question 1: What are the main benefits of a HELOC interest-only payment plan?

Interest-only payments initially reduce the monthly payment burden. This can provide short-term financial relief, potentially allowing for more cash flow. This flexibility is a critical consideration for individuals facing temporary financial strain or higher immediate expenses.

Question 2: What are the drawbacks of a HELOC interest-only payment plan?

The primary drawback is the accumulation of principal. This means the total interest paid over the life of the loan may substantially exceed the original loan amount. The increasing principal and interest accrued over time can result in a higher overall cost and pose a significant risk if not adequately planned for.

Question 3: How do interest rate fluctuations impact interest-only HELOC payments?

Variable interest rate HELOCs are susceptible to changes in market interest rates. Rising rates during an interest-only period can significantly increase the overall cost of borrowing. Conversely, a decline in rates might reduce monthly payments. Carefully assess the potential impact of rate fluctuations on the borrower's financial capacity.

Question 4: How does a HELOC interest-only plan compare to a standard repayment schedule?

Interest-only payments allow for lower initial monthly obligations, but this comes at the cost of a potentially higher total interest paid and an increased principal balance over time. Standard repayment methods include both principal and interest in each payment, reducing the principal balance more rapidly and, potentially, leading to lower total interest costs in the long term.

Question 5: What factors should be considered when assessing the suitability of an interest-only HELOC plan?

Critical factors include the borrower's ability to repay the accumulated principal, potential interest rate fluctuations, long-term financial stability, and a comparison with other repayment options. A comprehensive financial assessment, including realistic projections of income and expenses, is crucial for informed decision-making.

In conclusion, HELOC interest-only payments offer potential short-term financial relief but carry significant long-term financial implications. Thorough analysis, careful planning, and a realistic assessment of financial capacity are essential before opting for this repayment strategy.

The next section will delve deeper into different repayment strategies for HELOCs.

Conclusion

HELOC interest-only payments present a complex financial strategy with both short-term and long-term implications. The initial reduction in monthly payments is a key attraction, but the deferral of principal repayment leads to accumulating interest and a growing principal balance. This accumulation, coupled with potential interest rate fluctuations, significantly impacts the overall cost of the loan. A thorough evaluation of financial capacity, long-term goals, and a realistic repayment plan are essential. The strategy must align with the borrower's ability to repay the entire principal amount, including accrued interest, at a later date. Comparative analysis with other repayment methods is crucial to avoid significant financial strain in the future. Ultimately, a comprehensive understanding of the associated risks is paramount before opting for this repayment method.

Borrowers considering HELOC interest-only payments must prioritize a meticulous financial assessment. This assessment should encompass current and projected income, potential economic shifts, and contingency planning for unexpected financial needs. Transparent communication with lenders about repayment strategies is also advisable. The decision should not be driven solely by initial financial relief but rather by a comprehensive understanding of the long-term financial responsibilities. A proactive approach, characterized by careful planning and a clear understanding of the total loan cost, is essential for successful management of a HELOC with interest-only payments. Ultimately, responsible borrowing and a well-defined repayment strategy are key components of effective financial management.

You Might Also Like

Top 30 Out Of 6600: Must-See PicksBrian Gragnolati: Insights & Strategies For Success

Uncirculated Gold Dollars: Rare Finds & Investment

Darlene Nicosia: Expert Insights & Strategies

Starbucks Price-Earnings Ratio: 2023 Analysis & Insights

Article Recommendations

- Exploring The Life Of Jared Carrabis Wife A Deep Dive

- J Coles Influence On His Kids A Formal Exploration

- Zahn Mcclarnon Wife Insights And Personal Life