How are new financing options transforming the automotive industry? Cutting-edge methods for purchasing vehicles are reshaping the landscape.

Modern approaches to financing motor vehicles encompass a diverse range of innovative solutions. These solutions often involve leveraging technology to streamline the process, enabling quicker approvals and personalized financing options. For instance, online platforms are emerging as crucial intermediaries, offering comparative analysis of various loan terms and rates in a user-friendly manner. Furthermore, some models now incorporate flexible repayment schedules and consider factors beyond traditional credit scores to assess affordability, fostering greater accessibility to vehicle ownership. These new methods can include alternative financing options like vehicle leasing programs that offer tailored payment structures and potential for lower upfront costs. Examples can include partnerships with fintech companies and the utilization of advanced data analytics to assess and manage risk more effectively.

These novel financing strategies bring several advantages. They can potentially lower the barrier to entry for potential vehicle buyers, making ownership more attainable for a wider demographic. This broader accessibility can stimulate the market by encouraging greater consumer participation and potentially stimulating economic activity. Moreover, a more comprehensive and tech-driven approach can enhance efficiency in the financing process. This contributes to improved customer experience by streamlining the application process and enabling timely approvals. The financial models can also be more adaptive to individual circumstances, such as fluctuating incomes or specific financial needs, offering a more accommodating approach to vehicle ownership.

Moving forward, the exploration of these innovative financing methods promises to continue shaping the automotive industry. The next section will delve into the technological underpinnings of these advancements.

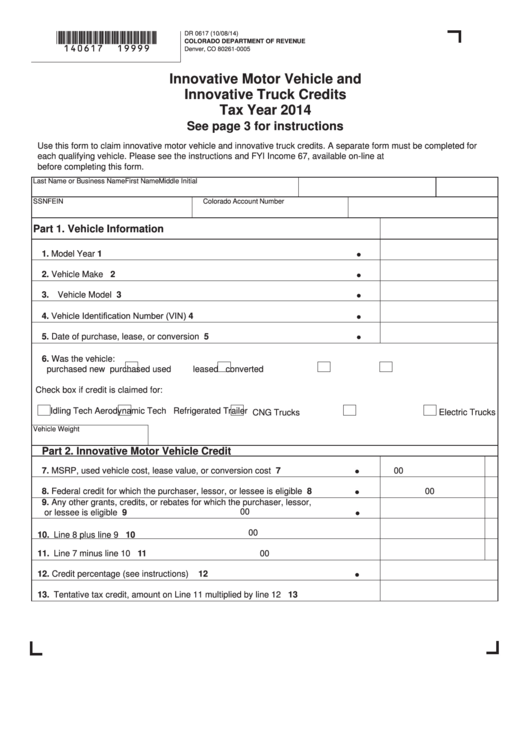

Innovative Motor Vehicle Credit

Innovative approaches to motor vehicle financing are transforming the automotive industry, impacting access, affordability, and efficiency. Key aspects are crucial for understanding this evolution.

- Technology

- Accessibility

- Affordability

- Transparency

- Risk assessment

- Flexibility

- Customer experience

- Data analytics

Innovative motor vehicle credit emphasizes leveraging technology for streamlined processes. Accessibility is enhanced by considering alternative credit scores and flexible repayment terms. Transparency in loan structures is crucial, enabling informed decision-making. Advanced risk assessment models ensure responsible lending practices. Flexibility in loan structures accommodates diverse financial situations. Focus on customer experience improves satisfaction and trust. Data analytics allows for more informed credit decisions and tailored financing options. These aspects together facilitate a more dynamic and inclusive approach to motor vehicle ownership. For instance, online platforms offering comparative loan options enhance transparency, while customized payment plans improve affordability. Ultimately, innovative models foster a more sustainable and accessible automotive market.

1. Technology

Technology plays a pivotal role in shaping innovative motor vehicle credit. The integration of digital platforms and sophisticated algorithms directly impacts every stage of the financing process, from application to disbursement and repayment. This evolution demands a thorough understanding of its multifaceted applications.

- Online Application and Assessment Platforms

Online platforms streamline the application process for potential borrowers. These platforms enable efficient gathering of required information, often eliminating the need for physical documentation. Automated systems for credit scoring and risk assessment leverage vast datasets to evaluate loan applications rapidly, leading to quicker approvals or denials. Examples include online comparison tools, allowing customers to assess various financing options and rates simultaneously. The result is increased convenience and transparency for consumers.

- Data Analytics for Risk Management

Sophisticated data analytics methods are used to refine risk assessment. These models go beyond traditional credit scores, incorporating various data points employment history, financial behavior patterns, and even social media activity to craft a more complete picture of the applicant's financial standing. The improved accuracy of risk assessment allows for potentially more inclusive and nuanced financing options. This approach enables financial institutions to assess risk more effectively.

- Mobile-First Lending Platforms

Mobile-first designs are becoming crucial for accessibility and convenience. Mobile applications offer on-the-go access to loan applications, account management, and payment options. This caters to the increasing prevalence of mobile device use in daily life. Borrowers can now track their loan progress and manage finances conveniently through mobile platforms.

- Blockchain Technology for Enhanced Security and Transparency

The application of blockchain technology can enhance security and transparency in loan processing. Its secure, decentralized nature potentially eliminates intermediary risks associated with traditional financial systems. This allows for faster transaction times and increased auditability, building trust and confidence in the system.

The convergence of these technological advancements signifies a shift toward a more automated, efficient, and potentially more inclusive motor vehicle credit system. Enhanced data analysis, online platforms, and mobile-first design contribute to a faster, more transparent, and convenient customer experience, while also enabling greater access to credit for a wider range of potential borrowers.

2. Accessibility

Accessibility in motor vehicle credit is fundamentally linked to innovative approaches. Traditional financing models often create barriers to ownership, particularly for individuals with limited credit histories or unique financial circumstances. Innovative credit models aim to mitigate these barriers by incorporating broader criteria for assessing creditworthiness and employing flexible repayment structures. For example, some models now consider factors beyond traditional credit scores, such as income stability, employment verification, and even evidence of responsible financial management. This shift reflects an understanding that creditworthiness is not a one-size-fits-all metric. Moreover, innovative payment plans, such as extended terms or variable interest rates tied to specific financial milestones, may offer greater affordability for a wider segment of the population.

The practical significance of enhanced accessibility is profound. A more inclusive approach to motor vehicle financing can stimulate economic activity by providing individuals with greater financial opportunities. Increased access fosters competition within the automotive industry, potentially driving down prices and expanding market reach. This, in turn, can create a more vibrant and resilient automotive sector. Furthermore, accessible financing can alleviate financial strain on individuals and families, improving their quality of life and overall well-being. The increased participation in the market that accessibility fosters can provide data-driven insights for future enhancements of financial products and services. Real-world examples of such success include programs offering tailored financing options for first-time buyers or individuals with specific financial needs, increasing the feasibility of vehicle ownership and participation in the economy.

Ultimately, fostering accessibility in innovative motor vehicle credit requires a commitment to multifaceted approaches. Financial institutions and policymakers must collaborate to create a framework that prioritizes inclusivity and affordability. This necessitates careful consideration of how existing financial structures can adapt to meet the evolving needs of consumers, ensuring a broader range of individuals can benefit from the innovations in the sector. Challenges remain, such as the need to educate consumers about the availability of these new options and ensuring the financial viability of these innovative lending models. Nevertheless, a broader focus on accessibility represents a crucial element in creating a more equitable and financially inclusive automotive landscape.

3. Affordability

Affordability is a critical component of innovative motor vehicle credit. Effective financing schemes must consider the financial realities of potential buyers. This includes not only the initial purchase price but also the ongoing costs associated with vehicle ownership, such as insurance, maintenance, and fuel. Innovative models strive to align loan terms with the long-term financial capacity of borrowers, reducing the risk of financial strain and promoting sustainable ownership. The goal is to make vehicle acquisition a viable option for a broader range of individuals, not just those with established credit profiles. This includes recognizing that financial situations and circumstances are complex and unique, not universally applicable. Programs offering flexible repayment options, lower interest rates, or extended loan terms directly address affordability concerns. Furthermore, innovative financing solutions may factor in potential future income or employment stability, broadening access to vehicle ownership.

Real-world examples of this principle in action include programs tailored for first-time buyers, offering reduced down payments or subsidized interest rates. Alternative financing options, like vehicle leasing, can lower the initial financial burden, providing potentially more manageable monthly payments. Innovative programs may incorporate income projections and assess financial stability beyond traditional credit scores to create more tailored payment structures. This approach recognizes that financial stability is a multifaceted measure, encompassing not just credit history but also factors such as consistent employment or verifiable income. These efforts result in more accessible vehicle ownership for a wider spectrum of potential buyers. Ultimately, affordable financing practices contribute to a healthier and more dynamic automotive market by stimulating demand and promoting consumer confidence in the products available.

The practical significance of integrating affordability into innovative motor vehicle credit is substantial. A more financially accessible market strengthens consumer confidence and promotes economic activity. Lower financial barriers can foster a broader range of participation in the automotive industry, leading to increased market stability and innovation within the sector. However, challenges remain. Ensuring the long-term financial viability of these innovative models requires careful consideration of risk management and potential repayment defaults. Regulatory frameworks may need adjustments to accommodate the evolving nature of financing and offer appropriate consumer protections. Additionally, educational outreach is important to equip consumers with the knowledge needed to understand and access these new financing options effectively.

4. Transparency

Transparency in motor vehicle credit is a crucial element of innovative financing models. Clear and readily accessible information about loan terms, interest rates, and associated fees is paramount. This fosters informed decision-making by potential borrowers, enabling them to compare different options effectively. Without transparency, borrowers may struggle to understand the full implications of a loan, potentially leading to unforeseen financial difficulties. Consequently, a transparent approach builds trust and reduces the likelihood of dissatisfaction or disputes down the line. This is particularly important as innovative methods often incorporate complex algorithms and data points, demanding clear communication of how these factors influence creditworthiness assessments.

Real-world examples highlight the practical significance of transparency. Online platforms that provide comprehensive comparisons of various financing options, detailing loan terms and interest rates across different lenders, exemplify this principle. Clear explanations of any hidden fees or charges associated with particular financing schemes contribute to a more equitable lending environment. Furthermore, transparent disclosure regarding the methodology used for credit risk assessment including which factors are considered and how builds consumer confidence and fosters a sense of fairness within the system. The implications extend beyond individual transactions, impacting market stability and investor confidence. By promoting transparency, the risk of predatory lending practices is mitigated and a fairer market is supported.

In conclusion, transparency is not merely a desirable feature but a fundamental component of innovative motor vehicle credit. It promotes informed decision-making, fosters trust between borrowers and lenders, and ultimately contributes to a more equitable and sustainable automotive finance market. While challenges, such as navigating complex algorithms and ensuring consistent disclosure standards across various platforms, remain, prioritizing transparency is essential for maintaining the integrity and broad adoption of these innovative financing methods. A robust commitment to transparency, coupled with readily accessible information and well-defined guidelines, ensures the long-term success and consumer acceptance of innovative motor vehicle credit models.

5. Risk Assessment

Accurate risk assessment is fundamental to innovative motor vehicle credit. Modern financing models face the challenge of evaluating creditworthiness in a rapidly evolving landscape, characterized by diverse financial profiles and technological advancements. Precisely assessing the risk associated with each loan application is crucial for the long-term financial health of both borrowers and lending institutions. Effective risk assessment underpins the viability of innovative lending strategies and plays a critical role in maintaining a stable and sustainable financial system within the automotive sector.

- Advanced Data Analytics

Contemporary risk assessment increasingly relies on advanced data analytics. Models consider a broader range of data points beyond traditional credit scores. These might include employment history, income stability, and patterns of financial behavior. Sophisticated algorithms assess this information to generate a more comprehensive risk profile. This approach allows lenders to identify potential risks and vulnerabilities more accurately, resulting in improved loan performance and reduced defaults. Real-world examples include predictive modeling techniques that assess the likelihood of loan repayment based on historical data and a variety of financial factors.

- Alternative Data Sources

Innovative risk assessment often incorporates alternative data sources. These may include digital footprint analysis, social media activity, and patterns of online financial behavior. These supplementary data sources provide a more holistic view of the borrower's financial circumstances. While utilizing alternative data presents challenges regarding privacy and potential bias, it can also reveal previously overlooked risk indicators, improving accuracy in loan decisions. Examples include using geolocation data to assess income stability or analyzing payment history across multiple platforms to gauge overall financial responsibility.

- Dynamic Credit Scoring Models

Risk assessment in innovative credit models frequently employs dynamic credit scoring models. These models adapt to changes in a borrower's financial situation over time. This is achieved through continuous monitoring and updates to the borrower's risk profile. The goal is to adjust creditworthiness ratings as the borrower's financial standing evolves, reflecting recent performance and current circumstances. This approach can provide more accurate and up-to-date assessments, improving the accuracy and relevance of risk analysis. Real-life examples include dynamic scoring models that respond to changes in employment status, income fluctuations, or significant financial milestones.

- Fraud Prevention and Detection

Robust risk assessment incorporates sophisticated techniques for fraud prevention and detection. Sophisticated algorithms analyze transaction data for anomalous activity and identify potential fraud attempts. These measures safeguard lenders against fraudulent applications and protect the integrity of the financing system. This proactive approach is essential in the context of innovative credit, where new technologies and avenues for fraud can emerge. Real-world examples of these techniques include the use of machine learning to detect patterns associated with fraudulent transactions and implementing multi-factor authentication procedures to enhance the security of the loan application process.

Effective risk assessment is not merely a technical exercise; it is a cornerstone of innovation in motor vehicle credit. The multifaceted approach, utilizing advanced data analytics, alternative data sources, dynamic models, and fraud detection measures, leads to a more comprehensive understanding of borrower risk. This, in turn, supports more responsible lending practices, fosters greater access to credit for a broader range of individuals, and ultimately promotes the sustainability of the entire automotive finance sector.

6. Flexibility

Flexibility is a defining characteristic of innovative motor vehicle credit. Modern financing models increasingly prioritize adaptable terms and conditions to accommodate diverse borrower needs and circumstances. This adaptability is crucial because fixed structures often fail to account for fluctuating incomes, unexpected life events, or evolving financial situations. Flexibility allows for a more nuanced approach, where loan terms can adjust to reflect individual circumstances, potentially reducing financial strain and promoting responsible borrowing.

The importance of flexibility in innovative motor vehicle credit is multifaceted. Variable interest rates tied to economic indicators or personal milestones allow for dynamic adjustments to monthly payments, aligning with fluctuating income patterns. Extended repayment periods, or the option to accelerate payments, offer borrowers greater control over their financial burden. Furthermore, flexible models may offer the choice between different repayment schedules to fit individual budgets, such as bi-weekly or even monthly payments that align with a borrowers paycheck cycle. In essence, flexibility transforms vehicle financing from a rigid, one-size-fits-all process into a more responsive and personal experience. Examples of this include models allowing borrowers to temporarily adjust their payment amounts during periods of financial hardship, without incurring significant penalties, a feature that enhances borrower satisfaction and loyalty.

The practical significance of understanding this connection is substantial. A flexible approach can significantly increase borrower participation in the automotive market. By offering terms that adapt to the realities of individuals' financial journeys, lenders increase the likelihood of loan repayment and reduce the incidence of default. This, in turn, strengthens the financial stability of both the borrowers and lending institutions. Moreover, a focus on flexibility signals a commitment to consumer well-being and responsible financial practices. However, the implementation of flexibility in innovative financing requires a careful balance between accommodating individual needs and maintaining the financial soundness of the loan structure. These factors need meticulous consideration to avoid compromising the stability of the overall system.

7. Customer Experience

A positive customer experience is increasingly recognized as a key differentiator in innovative motor vehicle credit. Effective customer service and a user-friendly approach to the financing process are crucial for attracting and retaining customers. A seamless experience, from initial inquiry to final loan disbursement, directly influences customer satisfaction and loyalty. Furthermore, a well-designed customer experience can contribute to a more positive perception of the entire industry.

Several factors contribute to a positive customer experience in the context of innovative motor vehicle credit. Intuitive online platforms, mobile applications, and readily available customer support channels are crucial. Prompt responses to inquiries, clear explanations of complex financial terms, and personalized service contribute significantly. Examples of successful implementation include streamlined online applications with automated notifications and secure payment options. Furthermore, proactive communication regarding loan status, timely updates, and readily accessible customer support channels minimize customer frustration and enhance trust in the process. The practical significance of this lies in increased loan application completion rates and reduced default rates, ultimately boosting financial stability for both borrowers and lenders.

The connection between customer experience and innovative motor vehicle credit is undeniable. A focus on enhancing the customer journey contributes to improved loan processing efficiency and increased borrower satisfaction. While challenges such as data security concerns and maintaining consistent customer service standards remain, prioritizing customer experience is vital in the competitive landscape of innovative financing. Sustained success in this area depends on ongoing assessment and adaptation to evolving customer expectations. Positive customer experiences are not simply a 'nice-to-have' but a crucial aspect of sustainable growth and success in the dynamic landscape of modern motor vehicle credit.

8. Data Analytics

Data analytics plays a pivotal role in shaping innovative motor vehicle credit. Its application significantly impacts various aspects of the financing process, from assessing creditworthiness to managing risk. Sophisticated data analysis allows for more accurate predictions of loan repayment potential, enabling lenders to make informed decisions. By evaluating a wider range of data points, lenders can identify individuals who might have been overlooked by traditional credit scoring methods. The result is a more comprehensive and potentially more equitable credit assessment system, extending access to a wider segment of the population.

The practical applications of data analytics are numerous. Algorithms can analyze vast datasets, encompassing credit history, income stability, employment data, and even patterns of online financial behavior. These analyses provide a deeper understanding of an individual's financial capacity and repayment likelihood, potentially revealing hidden factors that traditional approaches overlook. For instance, analyzing purchase history can provide insights into consistent financial habits, while employment patterns can indicate stability. This approach, utilizing complex statistical modeling and machine learning, can identify factors associated with responsible financial behavior, thereby allowing for a more tailored assessment of an applicant's creditworthiness. Real-world examples include the utilization of geolocation data to gauge income stability, providing a more accurate picture of a potential borrower's financial situation. Moreover, automated systems can quickly process applications and generate tailored loan offers that better match borrowers' financial situations.

The use of data analytics in motor vehicle credit is crucial for improved risk management. By identifying potential defaults early, lenders can mitigate their losses. The use of predictive models to estimate the probability of default enables proactively identifying high-risk borrowers, allowing for adjustments to loan terms or denial of applications altogether. While challenges like data privacy and potential biases in algorithms exist, the benefits of data-driven decision-making in a more inclusive and fair approach to vehicle financing are substantial. The improved accuracy in risk assessment supports the growth of innovative financing solutions, facilitating access to vehicle ownership for a more diverse population and strengthening the financial health of the automotive industry. Ultimately, data analytics drives a more efficient and equitable motor vehicle credit system, enhancing the entire landscape of automotive financing.

Frequently Asked Questions about Innovative Motor Vehicle Credit

This section addresses common inquiries regarding innovative motor vehicle credit, aiming to clarify key concepts and dispel potential misconceptions.

Question 1: What constitutes "innovative motor vehicle credit"?

Innovative motor vehicle credit encompasses financing methods that diverge from traditional models. These approaches utilize technology and data analytics for faster, more personalized financing solutions. This includes leveraging alternative data sources, employing dynamic credit scoring, and offering flexible repayment options tailored to individual financial circumstances. The overarching goal is to improve access to vehicle ownership for a wider range of individuals, while effectively managing associated risks.

Question 2: How do these innovative methods improve access to vehicle financing?

Innovative methods can improve access by considering factors beyond traditional credit scores. This may include evaluating income stability, employment history, and evidence of responsible financial habits. Flexible payment terms and potentially lower upfront costs can make vehicle ownership more attainable for individuals with limited or less-than-ideal credit histories. Online platforms streamline the application process, enabling quicker approvals and more transparent loan comparisons.

Question 3: Are these methods secure and reliable?

Robust risk assessment is integral to innovative financing models. Advanced data analytics and algorithms are designed to evaluate risk more accurately than traditional methods. Transparency in terms and conditions, coupled with security protocols, reduces the risk of fraud and ensures responsible lending practices.

Question 4: What are the potential downsides of innovative motor vehicle credit?

Potential downsides include the complexity of certain algorithms and the potential for bias in data-driven assessments. While these models aim for fairness, careful monitoring and regulation are crucial to mitigate biases and ensure equitable access. There may also be variations in the availability of these innovative credit models across different regions or financial institutions.

Question 5: How can consumers best prepare for applying for innovative motor vehicle credit?

Thorough research of different lenders and financing options is crucial. Understanding the terms and conditions associated with various products is paramount. Preparing comprehensive documentation pertaining to income, employment, and financial history, as required by the lender, will streamline the application process. Consumers should also be aware of potential fees and other associated costs to make informed decisions.

In conclusion, innovative motor vehicle credit aims to enhance access and affordability while managing risks effectively. Understanding the potential benefits and drawbacks is crucial for informed decision-making. The future of vehicle financing likely involves a greater integration of data analytics and flexibility in loan structures.

The following section explores the role of technology in supporting these advancements.

Conclusion

The evolution of motor vehicle credit reflects a shift towards a more data-driven and adaptable approach. Innovative models leverage technology to streamline processes, assess risk more effectively, and offer greater accessibility to a broader range of potential borrowers. Key elements of this transformation include enhanced transparency in loan structures, flexible repayment terms, and the integration of alternative data sources for risk assessment. These advancements have the potential to stimulate economic activity and broaden participation in the automotive market. However, responsible implementation remains crucial, particularly regarding risk management, bias mitigation, and equitable access across diverse populations.

The future of motor vehicle credit likely hinges on continued technological innovation and the development of more sophisticated algorithms for risk assessment. Maintaining consumer trust and transparency in the process will be crucial for widespread adoption. Continued adaptation and refinement of these innovative approaches will be essential to fostering a more inclusive and sustainable automotive financing landscape. Regulatory frameworks may need to adapt to accommodate the evolving nature of this market, ensuring equitable access and consumer protection. Ultimately, the ongoing evolution of innovative motor vehicle credit holds the potential to reshape the automotive industry, impacting both consumers and the economy.

You Might Also Like

Steve Gillis: Latest News & UpdatesUnveiling The Frenzy Of Evolution: A Deep Dive

243 Days In Months: A Quick Calculation

Clover Finance Price Prediction: Expert Insights & Potential

Best IPad Pro 12.9 2nd Gen Cases - Protective & Stylish

Article Recommendations

- Understanding Adam Walshs Age And Legacy

- Meet Amal Clooney The Dynamic Partner Of George Clooney

- Paul Walker And P Diddy A Deep Dive Into Their Connection