Is uninsured driving a risk in North Carolina? Understanding alternative coverage options is crucial for vehicle owners.

Insurance coverage for vehicles in North Carolina, specifically for drivers without ownership of the vehicle, is often a subject of concern. This alternative coverage, frequently offered by insurance providers, permits operation of a vehicle while legally ensuring liability protection. This coverage differs from standard policies by explicitly excluding the vehicle owner from the protection. It's a specific form of liability insurance designed to address situations where a driver is operating a vehicle without legally owning it. Examples include leasing situations or temporary use cases.

The importance of this insurance type lies in its provision of liability protection. Without it, a driver operating a vehicle in North Carolina risks facing significant financial repercussions if involved in an accident. Such protection, afforded by non-owner auto insurance, ensures financial responsibility for damages incurred by others in accidents. This is particularly pertinent in the context of vehicle operation involving individuals without a formal ownership stake.

This coverage is a crucial component of vehicle operation within North Carolina. A lack of adequate protection presents substantial financial exposure in case of accidents, highlighting the need for careful consideration when operating a vehicle.

NC Non-Owner Auto Insurance

Understanding non-owner auto insurance in North Carolina is essential for safe and responsible vehicle operation. This coverage safeguards against financial liabilities when operating a vehicle without legal ownership.

- Liability protection

- Temporary use

- Financial responsibility

- Accident coverage

- Legal compliance

- Third-party claims

- Vehicle operation

- Policy specifics

Non-owner insurance in NC addresses the need for liability coverage when operating a vehicle not legally owned. Temporary use, like a borrowed car or a vehicle used under a lease agreement, necessitates this type of insurance. Protecting yourself and other drivers is central to this coverage, as it ensures prompt and appropriate financial responses to accidents. Ensuring legal compliance is crucial; without this insurance, operators risk significant penalties. Policy specifics should be thoroughly reviewed for clarity on the coverage's limitations, exclusions, and any special circumstances that might apply. Examples include understanding deductibles, policy limits, and coverage gaps.

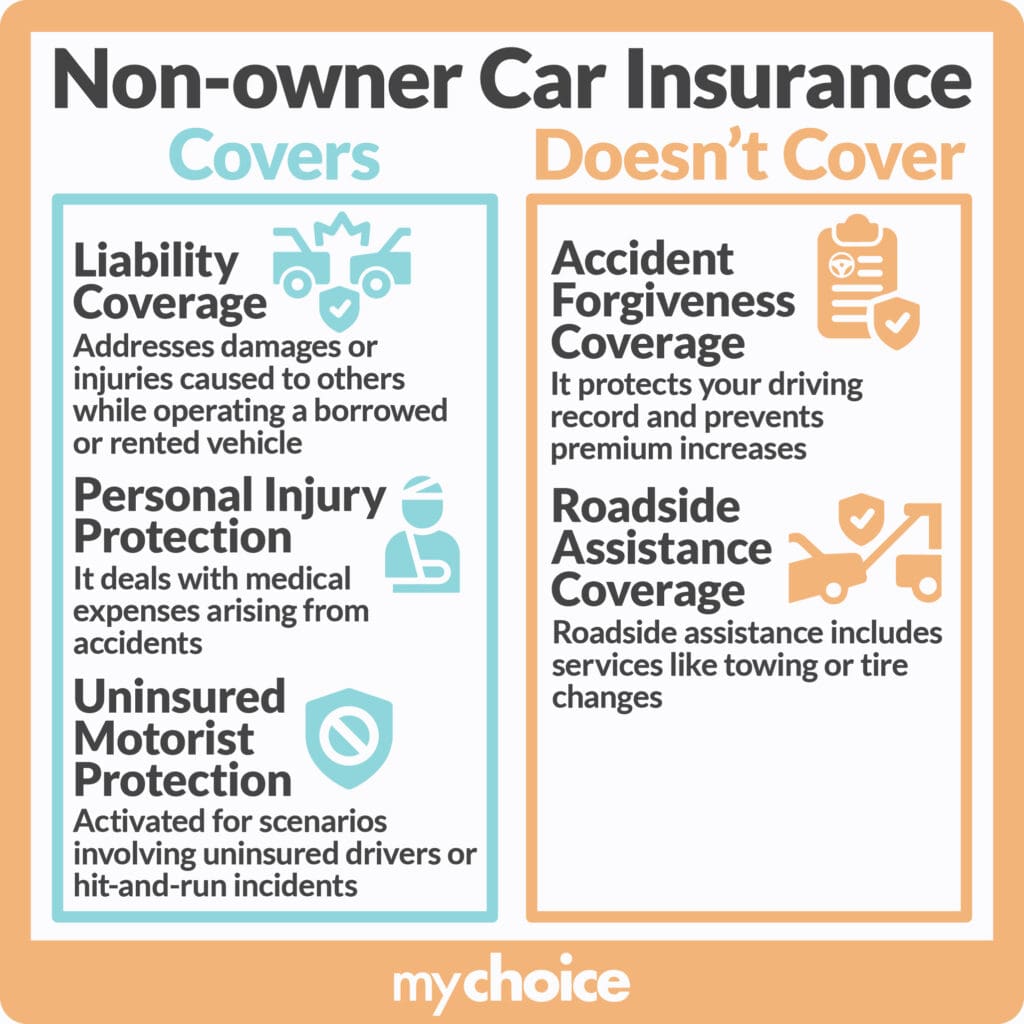

1. Liability Protection

Liability protection is a fundamental aspect of North Carolina non-owner auto insurance. It addresses the critical responsibility of financial compensation should an accident occur involving a vehicle operated by a person not legally owning it. The insurance policy, therefore, stands as a vital component for maintaining financial security and legal compliance.

- Scope of Coverage

The scope of liability protection in non-owner policies typically covers damages to other individuals or property. This often includes bodily injury and property damage. A key point to remember is that coverage specifically addresses the actions of the driver, not the vehicle owner. Examples include a situation where a driver, operating a car belonging to someone else, causes an accident. In such scenarios, the insurance steps in to handle third-party claims, shielding the driver from significant financial burden.

- Exclusions and Limitations

While providing protection, these policies often have exclusions or limitations. These may pertain to specific situations, such as pre-existing conditions or certain types of activities. Detailed policy review is crucial to ascertain the precise extent of coverage. Moreover, policy limits dictate the maximum amount of compensation the insurance can provide, representing a crucial factor for any driver.

- Legal Requirements and Implications

North Carolina laws mandate insurance coverage for all vehicle operators. Failure to maintain adequate liability protection can lead to serious penalties, including fines or legal repercussions. The insurance's role is to ensure the legal and financial responsibilities of the driver are met, regardless of vehicle ownership status.

- Relationship to Personal Responsibility

Liability protection in this context underscores personal responsibility. While the policy offers a safety net, it still emphasizes individual accountability for actions undertaken while operating a vehicle. The individual driver remains responsible for their actions and the coverage acts as a secondary financial safeguard.

In essence, liability protection within non-owner auto insurance in North Carolina is a critical component ensuring financial security and legal compliance. Drivers should thoroughly understand the specific details of their policies, including coverage limits and exclusions, to make informed decisions and protect themselves from potential financial burdens.

2. Temporary Use

Temporary use of a vehicle, a common occurrence in various scenarios, directly relates to non-owner auto insurance in North Carolina. This connection stems from the fundamental principle that individuals operating a vehicle not legally owned by them require specific liability coverage. Temporary use encompasses situations where a driver is not the vehicle's owner but is nonetheless responsible for its operation. This could involve borrowing a vehicle, using it under a lease agreement, or for short-term purposes.

The importance of temporary use as a component of non-owner insurance policies is evident in its practical application. Real-world examples include a family member borrowing a vehicle for a weekend trip, a friend using a vehicle for errands, or an employee operating a company vehicle under designated circumstances. In each case, the driver operating the vehicle is not the owner and is therefore not covered under the vehicle owner's policy. This absence of coverage highlights the critical need for separate insurance to address potential liabilities arising from accidents or damages incurred during temporary use. Without appropriate insurance coverage, those involved in temporary use face significant financial risks.

Understanding the connection between temporary use and non-owner insurance is essential for responsible vehicle operation. Proper insurance coverage safeguards individuals from substantial financial burdens and legal repercussions. Failure to obtain appropriate non-owner insurance during temporary use exposes the driver to significant legal and financial liabilities. This understanding is vital for both drivers and owners to protect their interests and maintain compliance with North Carolina's insurance requirements. The practical significance lies in avoiding costly mistakes and potential legal challenges when operating a vehicle not legally owned. Consequently, proactive measures, such as verifying appropriate insurance coverage for all temporary use situations, are crucial to ensure safety and legal compliance.

3. Financial Responsibility

Financial responsibility, a cornerstone of legal and ethical conduct, is inextricably linked to non-owner auto insurance in North Carolina. This connection stems from the inherent obligation to compensate for damages caused during vehicle operation. A driver operating a vehicle without ownership bears a financial responsibility that extends beyond the immediate parties involved. The potential for substantial liability necessitates insurance coverage. Without it, drivers risk facing significant financial burdens, potentially impacting personal finances and legal standing.

Consider a scenario where an individual, not the vehicle owner, is involved in an accident while driving a borrowed vehicle. Without adequate insurance, the individual becomes directly liable for any damages, encompassing medical expenses, property damage, and legal fees. This financial exposure highlights the critical role of non-owner auto insurance in mitigating potential financial ramifications. Such coverage acts as a safeguard against personal financial ruin. Further, it ensures responsible behavior on the road, minimizing the financial risk to all involved parties. This practical understanding underscores the necessity of insurance for drivers in various temporary situations, such as carpools, short-term rentals, and lease arrangements.

In conclusion, financial responsibility directly influences the necessity of non-owner auto insurance in North Carolina. The potential for significant financial liabilities associated with vehicle operation necessitates comprehensive coverage. Understanding this causal relationship is paramount for responsible drivers and vehicle operators, safeguarding personal finances and adhering to legal obligations. This connection underscores the importance of insurance as a critical component for mitigating the financial and legal risks inherent in operating a vehicle not legally owned. Failing to secure this insurance directly compromises financial responsibility, putting individuals at considerable risk in legal and financial spheres.

4. Accident Coverage

Accident coverage, a crucial component of North Carolina non-owner auto insurance, directly addresses the financial implications of accidents involving vehicles not legally owned by the operator. The causal link is straightforward: without this coverage, individuals operating such vehicles face substantial financial responsibility for any damages incurred in an accident. This responsibility encompasses costs associated with injuries to others, damage to property, and potential legal fees. The absence of accident coverage leaves individuals vulnerable to significant financial hardship.

Real-world examples illustrate the practical significance of this coverage. A teenager driving a friend's car without the necessary insurance, or an employee driving a company vehicle for a work-related errand, are situations where accident coverage is essential. An accident in these circumstances, without proper insurance, could result in crippling financial burdens for the driver. Medical expenses, property damage settlements, and legal costs can quickly escalate, placing the individual in a precarious financial position. The importance of comprehensive accident coverage cannot be overstated. This coverage protects not only the driver but also other parties involved in a potential accident. The presence of adequate coverage ensures compensation for all parties affected by an accident, supporting a fair and equitable outcome. Furthermore, comprehensive accident coverage demonstrates responsible vehicle operation, upholding the principle of financial accountability.

In conclusion, accident coverage is an indispensable aspect of non-owner auto insurance in North Carolina. Its significance lies in its ability to mitigate the substantial financial risks associated with accidents involving vehicles not legally owned. Without this coverage, drivers face significant financial exposure, and this understanding emphasizes the importance of securing appropriate insurance coverage when operating any vehicle, regardless of ownership status. This reinforces the necessity for responsible decision-making and legal compliance in vehicle operation.

5. Legal Compliance

Legal compliance is fundamental to non-owner auto insurance in North Carolina. Operating a vehicle without ownership necessitates adherence to specific legal requirements, and insurance plays a critical role in fulfilling these obligations. Failure to comply can lead to substantial penalties and financial repercussions, highlighting the importance of understanding the connection.

- Insurance Requirements by Law

North Carolina law mandates minimum insurance coverage for all vehicle operators. This includes drivers who do not own the vehicle. Non-owner insurance fulfills this legal requirement, ensuring financial responsibility in the event of an accident. Without this coverage, drivers could face fines, suspension of driving privileges, and potentially even legal action. Examples include drivers borrowing a vehicle from a friend or family member or those operating a vehicle under a lease agreement.

- Liability for Damages

Legal compliance extends to the responsibility for damages caused in an accident. Non-owner insurance policies help establish financial responsibility for injuries or property damage resulting from accidents. Without such insurance, the driver is legally liable for all associated costs, including medical bills, repair costs, and legal fees. This liability is irrespective of the vehicle's ownership. The insurance acts as a buffer against these potential financial burdens, reflecting a direct link between legal compliance and insurance.

- Avoiding Legal Penalties

Adherence to legal mandates regarding non-owner insurance is critical for avoiding legal penalties. Authorities can take action against drivers who operate a vehicle without sufficient coverage. These penalties can range from monetary fines to suspension or revocation of driving privileges. The consequences of non-compliance underscore the significant impact of meeting legal requirements for non-owner insurance.

- Protecting Third Parties

Legal compliance, in conjunction with non-owner insurance, protects third parties involved in an accident. Adequate insurance coverage ensures that individuals injured or suffering property damage receive compensation. Without insurance, third parties could face difficulty securing compensation from the driver. This protection is essential in maintaining societal order and financial accountability in accident situations.

In conclusion, legal compliance in North Carolina directly correlates with the necessity for non-owner auto insurance. This relationship is not just about personal financial responsibility but is a legal obligation that safeguards both the driver and third parties. Drivers operating vehicles they do not own must understand and comply with these regulations to avoid significant legal and financial repercussions. Compliance through appropriate insurance policies is thus critical to maintaining a safe and legally sound environment for all parties involved in vehicle operation.

6. Third-party claims

Third-party claims arise when an individual operating a vehicle, without legal ownership, causes harm or damages to others. This scenario directly implicates non-owner auto insurance in North Carolina. The crucial connection lies in the insurance policy's role in addressing financial liabilities stemming from such claims. Without adequate coverage, the individual is personally responsible for the financial consequences of a third-party claim, often exceeding available personal assets.

Consider an example: A teenager drives a vehicle belonging to a parent, and an accident occurs, resulting in injuries to another driver and significant property damage. Without non-owner insurance, the teenager is personally liable for the full extent of the claim. This could involve substantial medical bills, vehicle repair expenses, and potential legal fees. Non-owner insurance, in this context, acts as a critical safeguard, transferring financial responsibility from the driver to the insurance company, thus mitigating the personal financial repercussions of the claim. This protection directly safeguards the driver from potentially crippling financial burdens. Similar scenarios apply in situations involving leased vehicles or those operated under temporary use agreements. Understanding these relationships is crucial for personal financial well-being and legal compliance.

In summary, third-party claims directly necessitate non-owner auto insurance. This insurance acts as a crucial intermediary, handling financial obligations arising from such claims. Without this coverage, drivers face a severe risk of personal financial devastation. The need for non-owner coverage directly stems from the potential for significant financial burdens stemming from claims, which emphasizes the necessity for individuals operating vehicles they do not own to possess appropriate liability protection. This understanding underpins the importance of responsible vehicle operation and the crucial role of insurance in ensuring legal and financial compliance.

7. Vehicle Operation

Vehicle operation in North Carolina, especially concerning those without legal ownership, necessitates specific insurance considerations. The act of driving a vehicle inherently carries potential liabilities, and the absence of ownership significantly alters the associated risks. This necessitates a distinct type of insurance to address legal and financial responsibilities during such operation.

- Liability in Accidents

Vehicle operation inherently involves the potential for accidents. When an accident occurs, the driver, regardless of ownership, is legally responsible for damages incurred by others or their property. This responsibility extends to injuries sustained by individuals involved in the accident or damage to their belongings. Non-owner insurance policies directly address this liability by providing financial protection against potential claims from third parties. This is a crucial element in protecting the driver from the significant financial burdens that can arise from accidents.

- Temporary Use Scenarios

Many situations involve the temporary operation of vehicles not owned by the driver. Borrowing a car, using a vehicle under a lease agreement, or acting as a driver in carpooling arrangements are common examples. In these instances, the driver is not protected by the vehicle owner's insurance policy, necessitating separate coverage. Non-owner insurance specifically addresses the liability associated with these temporary operational circumstances, offering a safety net against potential financial ramifications.

- Legal Compliance and Penalties

North Carolina law mandates minimum insurance coverage for all vehicle operators. Failure to maintain appropriate coverage for vehicle operation, particularly for non-owners, can result in significant legal penalties. These penalties may include fines, suspension of driving privileges, or even legal action. Non-owner insurance ensures compliance with these legal mandates, thus safeguarding against such repercussions.

- Financial Responsibility and Protection

Vehicle operation, particularly in the absence of ownership, introduces substantial financial risks. Without insurance, drivers are solely responsible for any damages resulting from accidents. Non-owner insurance policies mitigate these risks by providing financial protection. This protection is crucial for preventing individuals from incurring substantial financial losses due to unforeseen accidents or claims, particularly when operating a vehicle not legally owned.

In conclusion, vehicle operation, encompassing diverse scenarios from temporary use to legal compliance, underscores the critical need for non-owner insurance in North Carolina. The specific legal and financial responsibilities associated with operating a vehicle necessitate appropriate coverage, safeguarding the driver and ensuring compliance with state laws. By understanding this connection, individuals can effectively manage the liabilities associated with vehicle operation, preserving their financial well-being and upholding legal obligations.

8. Policy specifics

Policy specifics are crucial details within non-owner auto insurance policies in North Carolina. They delineate the precise terms and conditions of coverage, impacting financial responsibility and legal compliance. Understanding these nuances is essential for responsible vehicle operation and avoiding potential financial liabilities.

- Coverage Limits

Policy limits define the maximum amount the insurance company will pay in a claim. These limits are expressed as monetary values for bodily injury and property damage. Understanding these figures is essential for assessing the financial protection afforded by the policy. For example, a policy with low limits might not adequately cover substantial damages in a serious accident. This limits the financial protection available to the insured and highlights the significance of selecting adequate limits given the potential risks associated with vehicle operation.

- Exclusions and Limitations

Exclusions outline situations where the policy does not provide coverage. These can encompass specific types of activities, locations, or circumstances. Understanding exclusions is vital for recognizing the policy's scope. For instance, a policy might exclude coverage for pre-existing medical conditions or driving under the influence. Knowing these exclusions is crucial to avoid misunderstandings and ensure that the policy genuinely addresses the potential risks of vehicle operation.

- Deductibles

Deductibles represent the amount an insured individual must pay out-of-pocket before the insurance company begins to pay. Different policy types have varied deductibles, impacting the financial burden in the event of a claim. A higher deductible signifies lower premiums, but it also increases the initial financial responsibility of the insured. Understanding deductibles helps individuals make informed choices about the level of premium they are willing to pay versus the financial responsibility they are prepared to shoulder.

- Definitions of Coverage

Clear definitions of terms like "vehicle," "insured," and "accident" are crucial. Inaccurate or vague wording can lead to disputes or denied claims. Carefully reviewing these definitions avoids misunderstandings regarding the policy's application. Precise language used in a policy ensures a clear understanding of what is and is not covered, preventing ambiguity and the possibility of disputes when a claim is made.

These policy specifics act as the backbone of non-owner auto insurance in North Carolina. By understanding coverage limits, exclusions, deductibles, and precise definitions, individuals can make informed decisions about their vehicle operation. Careful consideration of these factors is crucial for ensuring adequate protection against potential liabilities associated with operating a vehicle, thereby upholding legal obligations and personal financial security.

Frequently Asked Questions about NC Non-Owner Auto Insurance

This section addresses common questions about non-owner auto insurance in North Carolina. Clear understanding of these policies is crucial for responsible vehicle operation.

Question 1: What is non-owner auto insurance in North Carolina?

Non-owner auto insurance is a specific type of coverage for individuals operating a vehicle they do not own. This policy covers the driver's liability for accidents or damages caused while using the vehicle, including bodily injury and property damage. It protects the driver from personal financial responsibility, but details vary by policy.

Question 2: Why is non-owner auto insurance necessary?

North Carolina law requires all drivers to maintain minimum liability insurance coverage. Non-owner insurance ensures compliance with these legal mandates. Without it, drivers face significant legal penalties and personal financial risk in the event of an accident.

Question 3: Who needs non-owner auto insurance?

Individuals operating a vehicle not legally owned by them need non-owner insurance. This includes those borrowing vehicles, using them under lease agreements, or involved in carpools. All parties operating the vehicle, regardless of their relationship to the owner, require this coverage.

Question 4: How much does non-owner auto insurance cost?

The cost of non-owner auto insurance varies based on factors such as the driver's driving record, the vehicle's model year and safety features, and the coverage limits. Insurance providers use specific criteria to assess risk and determine premiums. Contacting multiple insurance providers is advisable to compare prices and coverage.

Question 5: What are the limitations of non-owner insurance?

Non-owner policies typically have limitations. These may include specific exclusions for certain activities, driving locations, or pre-existing conditions. Detailed review of the policy specifics is paramount to understand the full scope of coverage. Policies may not provide coverage in all situations.

Understanding these FAQs provides a foundation for making informed decisions about non-owner insurance in North Carolina. Consult with insurance professionals for personalized advice regarding specific situations and coverage needs.

Proceed to the next section

Conclusion

This exploration of NC non-owner insurance highlights the critical need for comprehensive coverage when operating a vehicle not legally owned. Key takeaways emphasize the legal requirement for insurance, regardless of ownership status, and the significant financial responsibility associated with vehicle operation. The importance of accident coverage, liability protection, and the potential for third-party claims are underscored, emphasizing the necessity of understanding policy specifics, including limits, exclusions, and deductibles. The discussion underscores the practical implications for temporary use scenarios, carpools, and leased vehicles, stressing the need for appropriate protection against potential financial burdens. Ultimately, compliance with North Carolina's insurance mandates is crucial to ensure safety, uphold legal obligations, and safeguard personal financial well-being.

In conclusion, navigating the complexities of vehicle operation without ownership necessitates a proactive approach to insurance. Understanding policy specifics and seeking professional guidance when necessary is paramount for responsible drivers. Failure to secure appropriate coverage exposes individuals to substantial legal and financial risks, necessitating careful consideration of this essential aspect of vehicle operation in North Carolina. Thorough research and informed decisions regarding insurance coverage remain critical for all drivers. This underscores the paramount importance of diligent planning for any situation involving the operation of a vehicle in the state.

You Might Also Like

Dormant Companies: Finding Hidden OpportunitiesUnbelievable Deals! 5 Items Under $10,000

Kent Masters: Top Players & Events

Rare Flipper Quarters: Value & Collecting

Atreca Inc. Solutions: Innovation & Growth

Article Recommendations

- Angie Hermon The Rising Star In The Entertainment Industry

- The Enigmatic Simon Baker Hollywoods Charismatic Star

- Katt Williams Family Adorable Pictures Moments