What are the implications of certificate of deposit (CD) interest rates offered by Dr. Bank? How can these rates affect investment strategies?

Certificate of deposit (CD) rates offered by Dr. Bank represent the interest percentage a depositor earns on a time deposit. These rates vary based on factors such as the deposit term (length of time the funds are held in the account), the principal amount, and overall market conditions. For instance, a three-year CD might offer a higher rate than a one-month CD. An account with a larger principal amount could potentially attract a slightly better interest rate. These rates are often crucial for individuals and businesses aiming to preserve capital and generate passive income.

The importance of these rates stems from their direct impact on the return on investment (ROI). Higher rates translate to more favorable returns. Historically, CD rates have fluctuated with broader economic trends. Periods of low interest rates are often observed during economic downturns, while rates might increase during periods of growth. Understanding the prevailing CD rates at Dr. Bank, and how they compare to market averages, is critical for effective financial planning and achieving desired financial goals. Knowing these rates allows comparison shopping and enables informed decisions regarding investments, considering the risks and expected returns. The implications are particularly significant for individuals with substantial capital or those seeking to generate steady income from investments over time.

Let's now delve into the specifics of CD rates at Dr. Bank. This exploration will consider factors impacting rates, investment strategies for maximizing returns, and the potential risks associated with this particular financial product. Understanding these details is crucial for those considering CDs as part of their investment portfolio.

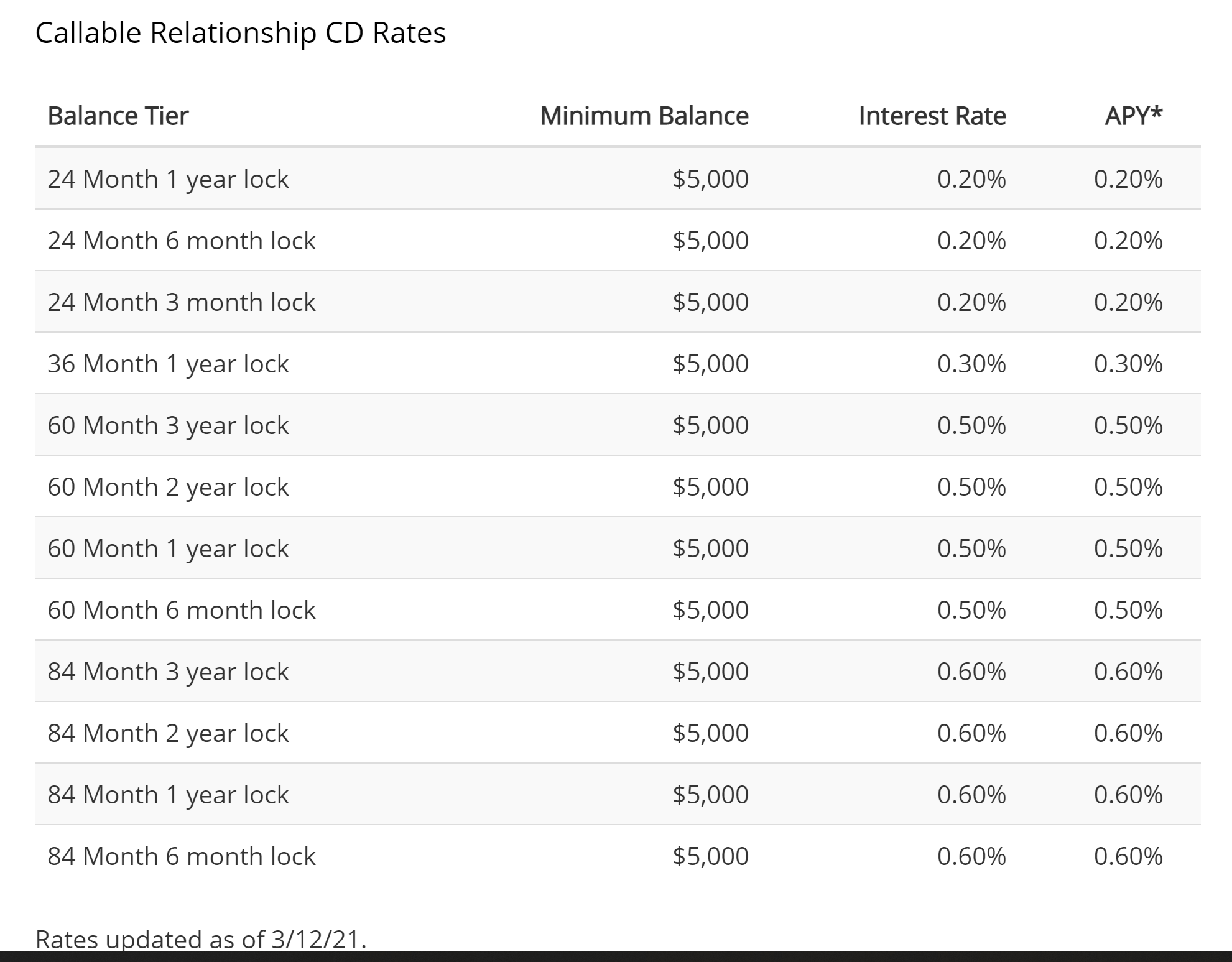

Dr. Bank CD Rates

Understanding Dr. Bank's certificate of deposit (CD) rates is crucial for informed investment decisions. These rates directly affect returns and should be considered alongside other financial factors.

- Interest Rates

- Maturity Dates

- Principal Amounts

- Market Conditions

- Term Lengths

- Fees and Penalties

- Account Types

Dr. Bank's CD rates are influenced by a complex interplay of factors. Interest rates, determined by market forces, are a primary driver. Different maturity dates, term lengths, and principal amounts affect the specific rate offered. Economic conditions and the prevailing interest rate environment also shape CD rates. Understanding fees and penalties associated with early withdrawals is critical. Various account types, such as high-yield CDs, might offer competitive rates. A thorough analysis of these factors provides a complete picture, enabling a comparison with alternative investments and the evaluation of appropriate strategies for maximizing returns. For example, a five-year CD with a high principal could yield a higher rate than a short-term CD with a smaller principal amount.

1. Interest Rates

Interest rates are a fundamental component of Dr. Bank's CD rates. The relationship is direct and consequential. Higher prevailing interest rates in the broader market typically correlate with higher CD rates offered by Dr. Bank. This correlation reflects the interplay of market forces. When borrowing costs rise, institutions like Dr. Bank, seeking to attract deposits, may offer more competitive interest rates on their CDs. Conversely, low market interest rates often lead to lower CD rates. The bank's strategy aims to balance attracting deposits with maintaining profitability.

For instance, during periods of economic uncertainty or recession, interest rates often fall. In response, Dr. Bank might lower their CD rates to attract and retain depositors. Conversely, in periods of economic growth or inflation, interest rates tend to increase. This frequently results in higher CD rates offered by Dr. Bank to compete effectively in the market. The bank's rate adjustments are a crucial reflection of its position within the broader financial landscape and its competitiveness. Understanding these fluctuations is vital for potential investors to make sound financial decisions.

In summary, the connection between interest rates and Dr. Bank's CD rates is intrinsically linked. Understanding the prevailing interest rate environment is crucial for evaluating the potential returns of Dr. Bank CDs. While Dr. Bank's specific rates are influenced by internal factors, the broader market trend plays a significant role. Investors should analyze both the current interest rate climate and Dr. Bank's specific CD offerings to make informed choices aligning with their investment goals.

2. Maturity Dates

Maturity dates significantly influence certificate of deposit (CD) rates at Dr. Bank. The length of time funds remain invested directly impacts the interest rate offered. This relationship is a crucial factor for investors to consider when assessing potential returns.

- Impact on Interest Rates

CDs with longer maturity dates generally offer higher interest rates. This reflects the increased risk for the financial institution, as funds are committed for a longer period. Conversely, shorter-term CDs typically yield lower interest rates. This difference in risk and return is fundamental to understanding how maturity dates affect CD rates. A one-year CD will typically have a lower rate than a five-year CD. This relationship is essential for investors to evaluate the potential return for a given level of risk. Market conditions, of course, still play a significant role.

- Liquidity Considerations

The maturity date dictates the availability of funds. Investors need to consider the trade-off between potential return and liquidity. Shorter-term CDs offer higher liquidity, allowing for easier access to funds. Longer-term CDs typically offer higher rates but also require funds to be committed for a longer period, limiting immediate access. Investors must weigh their liquidity needs against the potential for increased returns from a longer-term commitment.

- Matching Investment Goals

Investors should align the maturity date of their CD with their financial goals. For example, a CD with a maturity date aligned with a specific future expense, such as a down payment on a house, provides a dedicated savings plan. A shorter-term CD might be more appropriate for an individual aiming to have funds available for immediate use. Matching the investment horizon with the maturity date is critical for maximizing returns and ensuring funds are available when needed.

- Market Volatility Considerations

Changes in market conditions can impact CD rates over time. Investors should consider the potential for market volatility, especially with longer-term CDs. Fluctuations in interest rates can affect the overall yield achieved, especially if the CD's maturity date is in a period of significant market uncertainty.

In conclusion, the interplay between maturity dates and CD rates at Dr. Bank requires careful consideration. Understanding the relationship between these factors is critical to evaluating the potential return and the liquidity needs of the investor. The maturity date of a CD significantly impacts the overall investment strategy and the potential for return, demonstrating a direct link between commitment period and the interest rates offered. Investors must carefully analyze their specific financial goals and the expected market conditions when selecting a CD with a particular maturity date to maximize returns and ensure funds are available when needed.

3. Principal Amounts

The principal amount deposited for a certificate of deposit (CD) at Dr. Bank directly influences the interest rate offered. This relationship is a crucial component in evaluating CD investment opportunities. Understanding this connection is essential for optimizing returns and aligning investment strategies with financial objectives.

- Impact on Offered Rates

Larger principal amounts generally attract more favorable interest rates. This reflects the increased commitment of funds and the potential increased risk for the institution. Dr. Bank, like other financial institutions, may offer a competitive interest rate to attract larger deposits. This is often done by offering tiered rates, where different rates apply to different principal amounts. Examples of tiered rates might involve a higher rate for deposits of $50,000 or more compared to deposits below that threshold. Such differentiated rates are common industry practice.

- Minimizing Effects of Rate Fluctuations

For substantial principal amounts, the potential impact of interest rate fluctuations can be minimized. Larger deposits often result in a more significant investment return, even during periods of declining rates. This is due to the compounding effect of the larger initial sum. This characteristic can be particularly beneficial during periods of uncertainty. While fluctuations remain a factor, a larger investment cushion can sometimes mitigate the impact.

- Relationship to Investment Goals

Investors should carefully consider their investment objectives when selecting the principal amount. Matching the principal amount to anticipated financial goals or expenditures is vital. A substantial deposit might align with long-term savings goals. Smaller deposits might better support short-term objectives or ongoing financial needs.

- Comparison with Other Investment Options

Investors should evaluate the relationship between principal amount and potential return alongside other investment options. A complete financial strategy requires considering expected returns from CDs compared to other avenues, such as stocks or bonds. This comparison is crucial to optimize the allocation of investment capital.

In conclusion, the principal amount plays a significant role in determining interest rates for CDs at Dr. Bank. Larger principal amounts typically result in more favorable rates, which can enhance overall returns. However, investors should meticulously assess their financial objectives, consider other investment opportunities, and compare potential returns across different options to make informed decisions.

4. Market Conditions

Market conditions exert a considerable influence on certificate of deposit (CD) rates at Dr. Bank. The relationship is fundamentally causal; shifts in the broader economic environment directly impact the interest rates offered on CDs. This influence is substantial, as market forces determine the prevailing borrowing costs and the overall demand for savings instruments. Understanding this connection is crucial for effective financial planning and investment strategy.

Several key market factors influence Dr. Bank's CD rates. Interest rate adjustments by central banks, often in response to inflation or economic downturns, are a primary driver. Increased inflation frequently leads to higher interest rates to curb spending and encourage savings, thus impacting the rates offered on CDs. Conversely, during periods of economic recession or stagnation, central banks might reduce interest rates, affecting CD rates downward. Moreover, investor confidence and the overall risk appetite of the market play a role. Periods of market uncertainty or heightened risk aversion might decrease demand for riskier investment options like CDs and thus impact the offered interest rates. Supply and demand within the broader financial market also plays a role. If the demand for CDs increases due to investor confidence, Dr. Bank might be compelled to adjust rates accordingly.

Consider, for example, a period of rising inflation. Central banks react by raising benchmark interest rates. This ripple effect leads to higher borrowing costs for all financial institutions, influencing the rates offered on CDs. Conversely, during a period of economic downturn, lowered interest rates might decrease the attractiveness of CDs as a return-generating investment compared to other, potentially riskier, opportunities. Historically, correlation between market conditions and CD rates is not absolute and can be influenced by individual bank strategies, but the overall connection is a significant component of financial analysis. This understanding is essential for investors to adapt their investment strategies accordingly, enabling informed decision-making when selecting CD rates.

5. Term Lengths

The duration of a certificate of deposit (CD) significantly impacts the interest rate offered by Dr. Bank. This relationship is fundamental to understanding CD investments. Longer term commitments, generally, attract higher interest rates. This is a direct consequence of the increased risk for the financial institution; funds are committed for a longer period, potentially impacting their liquidity and flexibility. Conversely, shorter-term CDs typically yield lower interest rates. This difference reflects the inherent trade-off between potential return and the duration of the commitment.

Examining real-world examples, a five-year CD often carries a higher interest rate than a one-month CD. This higher rate compensates the depositor for tying up capital for a longer period. The bank, in turn, benefits from the consistent deposit and can deploy these funds for longer-term loans or investments. Conversely, a short-term CD might be beneficial for individuals seeking immediate access to funds. However, the return potential is comparatively lower. An understanding of this direct correlation between term length and rate is crucial for investment decisions, enabling investors to select CDs aligned with their financial goals and time horizons. For instance, a business saving for equipment in five years may opt for a longer-term CD with higher interest rates, whereas a household with an immediate need for funds might favor a shorter-term CD with lower rates, emphasizing the importance of aligning term length with personal financial strategies.

In conclusion, the term length of a CD is a pivotal determinant of the interest rate offered by Dr. Bank. A deeper understanding of this relationship is essential for investors to choose CDs that align with their financial goals and time horizons. Investors should meticulously analyze their individual needs and carefully assess the trade-off between potential returns and the duration of commitment. This knowledge is fundamental to optimizing investment strategies and ensuring that financial decisions are well-informed, given that market conditions and the institution's specific rate structures still influence the actual rate offered.

6. Fees and Penalties

Understanding fees and penalties associated with certificates of deposit (CDs) at Dr. Bank is essential when evaluating the overall value proposition. These provisions directly impact the net return and should be thoroughly considered alongside interest rates and other terms. Ignoring these conditions can lead to unforeseen financial consequences.

- Early Withdrawal Penalties

Early withdrawal penalties are common stipulations in CD agreements. These penalties are designed to incentivize adherence to the agreed-upon term and provide stability to the institution. They are expressed as a percentage of the principal amount or a fixed fee, and the percentage or amount often increases with the length of the remaining term. For instance, a CD with a three-year term might incur a penalty of 3% of the principal amount for early withdrawal. If a depositor withdraws funds before the maturity date, the penalty must be considered a deduction from the accrued interest. These penalties mitigate the risk of early withdrawals, ensuring a predictable return for the bank. This characteristic is vital for maintaining the institution's financial health and stability.

- Account Fees

Certain CDs may come with associated account fees, such as monthly maintenance fees or fees for specific services. These fees must be factored into the overall cost of the CD. The specifics should be clearly outlined in the agreement terms. For example, some institutions may charge a monthly fee for certain account types or for electronic fund transfers. The added costs influence the net return, potentially altering the attractiveness of the investment.

- Prepayment Fees

Prepayment fees differ from early withdrawal penalties, often applying when the entire principal amount is paid before the maturity date. These fees are intended to compensate for potential losses the institution incurs when funds are repaid earlier than anticipated, thus affecting the net gain from the CD. The associated fees are typically outlined in the CD agreement and might be calculated as a percentage or fixed amount. Evaluating this additional cost is crucial to a thorough analysis of the investment.

- Impact on ROI

Fees and penalties have a direct impact on the return on investment (ROI) from a CD. Evaluating the potential cost of these provisions is essential to compare different CD options and determine the most financially advantageous choice. A comprehensive evaluation should consider not only interest rates but also potential penalties and associated fees to ascertain the true profitability of a CD investment. Ignoring these charges can lead to significant underestimation of the actual cost of an investment, thus impacting overall profitability.

Ultimately, the fees and penalties associated with Dr. Bank CDs must be meticulously evaluated alongside the interest rates and other terms. A comprehensive understanding of these provisions is crucial for achieving a clear view of the investment's true cost and potential returns. A detailed analysis of these provisions is crucial for maximizing the financial benefits of a CD investment. Comparing different CDs across various financial institutions, taking these fees and penalties into consideration, is necessary for an informed decision.

7. Account Types

Different account types offered by Dr. Bank can significantly influence certificate of deposit (CD) rates. Account structures, such as high-yield CDs or specific tiered options, often lead to varying interest rates. The relationship is direct and consequential; certain account types are designed to attract deposits or cater to specific financial needs, which in turn impacts the rate offered. These varying rates reflect the balance between attracting deposits and maintaining profitability, a common practice in the financial industry.

For example, a high-yield CD account might offer a higher interest rate than a standard CD account. This differentiation encourages depositors to choose high-yield options, attracting deposits and potentially leading to more favorable rates. Conversely, simpler CD accounts may offer lower rates but often have more straightforward terms and conditions. Further, specific tiers within account types, such as CDs with higher principal amounts, might come with preferential rates. These distinctions in account types provide flexibility for depositors, allowing them to choose accounts best suited to their financial goals. A business aiming for high-volume savings might prefer high-yield accounts, whereas an individual seeking a simpler savings structure might choose a standard CD. This individualized approach to account structures is a core component of competitive banking practices. The practical significance of this understanding allows depositors to select the most suitable account type, maximizing returns and aligning investment strategies with specific financial objectives.

In summary, the account type is a critical consideration when evaluating Dr. Bank's CD rates. Different structures, including high-yield and tiered options, directly impact the offered interest rate. Understanding these distinctions allows depositors to select the most suitable account type to meet their financial needs and maximize potential returns. The choice of account type effectively determines the specific CD rates available, highlighting the importance of careful consideration for optimizing financial outcomes. Carefully reviewing the terms of each account is vital to achieving the desired outcomes.

Frequently Asked Questions about Dr. Bank CD Rates

This section addresses common inquiries regarding certificate of deposit (CD) rates offered by Dr. Bank. Accurate information is crucial for informed investment decisions. Please note that specific rates are subject to change and should be confirmed directly with Dr. Bank.

Question 1: What factors influence Dr. Bank's CD rates?

Dr. Bank's CD rates are determined by a combination of factors, including prevailing market interest rates, the term length of the CD, the principal amount, and overall economic conditions. Changes in these factors can lead to adjustments in CD rates.

Question 2: How do term lengths affect CD rates?

Longer-term CDs typically offer higher interest rates than shorter-term CDs. This reflects the increased risk for the financial institution, as funds are committed for a longer period. The longer the commitment, the greater the potential return offered to incentivize the investment.

Question 3: Are there any fees associated with CDs at Dr. Bank?

Yes, some CDs may have associated fees. Early withdrawal penalties are common and may apply if funds are withdrawn before the maturity date. Account fees, such as monthly maintenance fees or fees for specific services, may also apply. It is crucial to review the terms and conditions carefully to understand these potential fees.

Question 4: How do principal amounts affect CD rates?

Larger principal amounts generally attract more favorable interest rates. This reflects the increased commitment of funds and the potential for greater returns to the institution. While not always a direct correlation, larger deposits often result in better interest rates.

Question 5: What are the implications of market conditions on Dr. Bank CD rates?

Market conditions, such as prevailing interest rates, inflation, and economic trends, significantly impact CD rates. Changes in these conditions will influence the rates Dr. Bank offers. Investors should remain informed about current market trends to make well-considered decisions.

Understanding these factors enables informed decision-making for individuals and businesses considering CD investments offered by Dr. Bank. Always consult with a financial advisor if needed.

This concludes the frequently asked questions section. The next section will explore investment strategies involving CDs.

Conclusion

This analysis explored the multifaceted factors influencing Dr. Bank's certificate of deposit (CD) rates. Key determinants included prevailing market interest rates, the term length of the deposit, the principal amount, and economic conditions. The relationship between these factors is complex and dynamic, requiring careful consideration. Understanding the interplay of these elements is crucial for evaluating potential returns and aligning investment strategies with financial objectives. The analysis highlighted the importance of considering not only the stated interest rate but also associated fees, penalties, and the specific account type. This comprehensive approach facilitates informed decisions regarding CD investments offered by Dr. Bank.

Ultimately, the decision to invest in Dr. Bank CDs necessitates a thorough evaluation of individual financial goals and risk tolerance. Investors should carefully compare CD options, considering market conditions and the institution's specific terms. By understanding the interplay of these factors, investors can make well-informed decisions and potentially maximize the returns on their investments. A financial advisor's guidance can further enhance the decision-making process.

You Might Also Like

Andrew Chen Net Worth 2023: Updated FiguresValerie Kay Age: Uncovering The Details

Uncommon & Valuable Quarters: Find Rare Coins

Safely Microwaving Weed: Quick Guide & Tips

Kellogg's Net Worth 2024: Company's Value Revealed

Article Recommendations

- Exploring Gizelle Bryants Ethnicity A Deep Dive Into Her Heritage

- Meet Zach Tops Stunning Wife Discover Her Beauty And Style

- Discovering Mr Ballens Wife An Indepth Look At Their Relationship